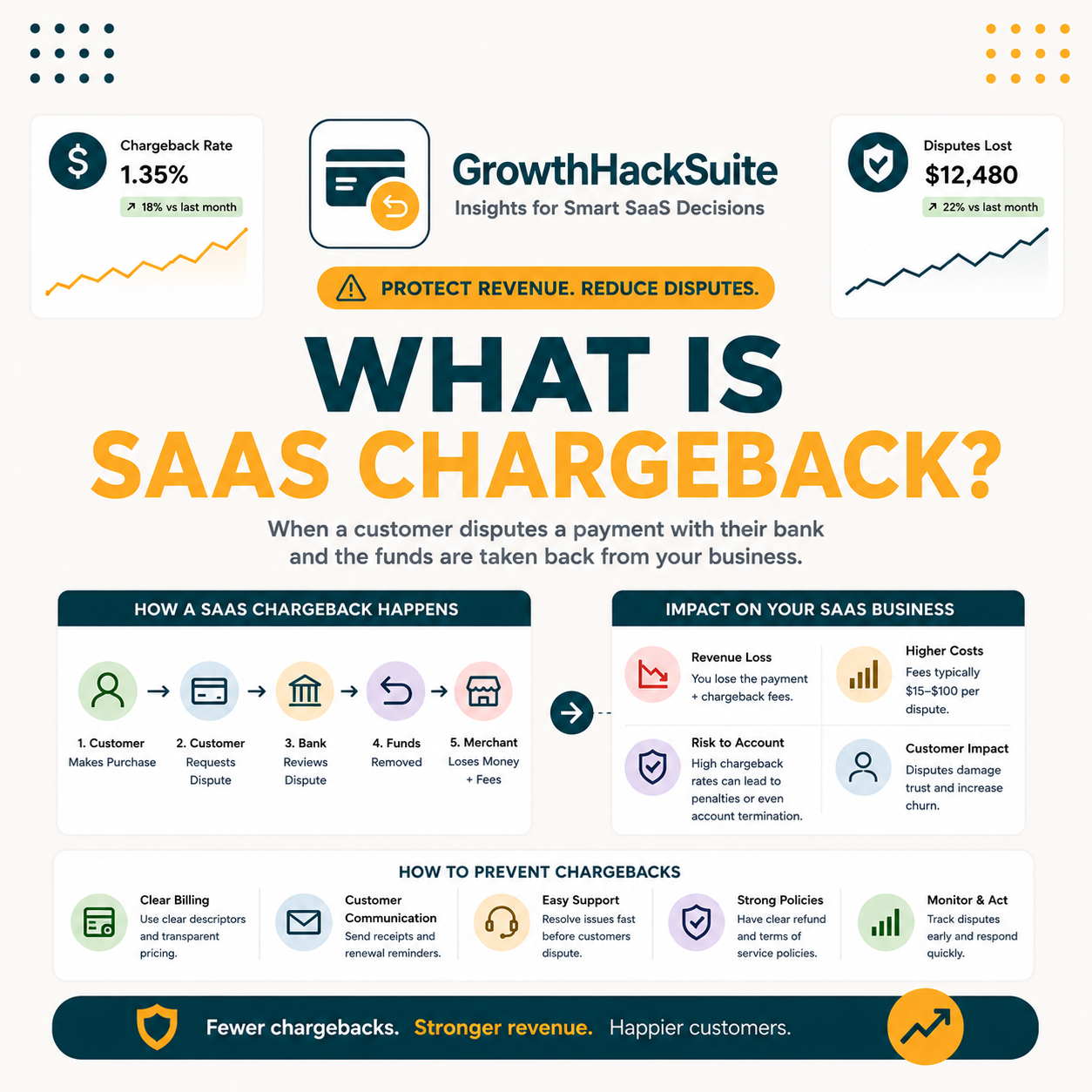

A SaaS chargeback is a bank-enforced payment reversal that bypasses the vendor, governed by Visa and Mastercard dispute rules. Unlike a refund, a chargeback lets cardholders reclaim funds when a vendor refuses to act. For B2B teams using email tools like Hunter.io, knowing the five justified scenarios, the 60-to-120-day filing window, and the account termination risk matters before escalating.

What Is SaaS Chargeback? Core Definition for B2B Sales and Marketing Teams

A SaaS chargeback occurs when a subscriber contacts their credit card issuer to reverse a payment made to a software vendor, without the vendor’s consent. The bank investigates, temporarily credits the cardholder, and requests a response from the merchant. If the vendor cannot prove the charge was valid, the reversal becomes permanent. For B2B teams on monthly email tool subscriptions, chargebacks are a last resort after refund requests fail.

Source: Visa Dispute Resolution Guidelines; Mastercard Chargeback Guide 2025

“A chargeback is a return of money to a payer of a transaction, especially a credit card transaction.”

: Wikipedia: Chargeback

SaaS chargeback volume has risen alongside subscription adoption: as more B2B teams pay monthly for tools, billing disputes involving credit card networks have become a standard escalation path alongside traditional vendor support channels.

How Does SaaS Chargeback Actually Work? The Technical Mechanism Explained

A SaaS chargeback moves through five distinct stages from the moment a cardholder contacts their bank to the moment funds are settled. The entire process typically takes 30 to 90 days, during which the bank provisionally credits the cardholder while the vendor prepares a rebuttal. Vendors who fail to respond within the deadline, usually 20 to 45 days, automatically lose the dispute.

- Dispute initiation: The cardholder contacts the issuing bank and cites a specific reason code. Visa and Mastercard maintain standardized codes covering fraud, service failures, and processing errors.

- Provisional credit: The bank temporarily returns the funds to the cardholder while the investigation runs. The vendor’s account is simultaneously debited and a chargeback fee of $25 to $100 is applied.

- Retrieval request: The vendor receives a notification and is asked to provide documentary evidence: invoices, service delivery logs, usage records, and any prior refund communications.

- Vendor rebuttal: A compelling rebuttal includes proof of delivery, signed terms of service, cancellation timestamps, and correspondence showing the vendor attempted resolution before the dispute.

- Final ruling: The card network reviews both sides and issues a binding decision. If the vendor wins, the provisional credit reverses. If the cardholder wins, the vendor permanently loses the funds plus fees.

Vendors who accumulate chargeback rates above 1% of monthly transactions enter card network monitoring programs, which can ultimately result in account termination with their payment processor.

What Are the Top 5 Use Cases for SaaS Chargeback in B2B Sales?

Chargebacks are legally justified in specific scenarios where the vendor either failed to deliver, billed in error, or refused a reasonable refund request. Filing outside these scenarios, sometimes called “friendly fraud,” exposes the buyer to account bans and card restrictions. Five scenarios consistently produce successful chargeback outcomes for B2B teams.

Five use cases below cover the scenarios where SaaS chargebacks reliably succeed in B2B disputes.

- Unauthorized billing after cancellation: A subscription continued charging after the customer submitted cancellation confirmation. Documentation of the cancellation timestamp and subsequent charges is the strongest chargeback evidence.

- Duplicate charge: The vendor billed the same invoice twice in the same billing cycle. Card networks classify duplicate charges as processing errors with high cardholder win rates.

- Service not delivered: The SaaS tool was inaccessible for a material portion of the billing period, and the vendor declined to issue a credit. Downtime logs from third-party monitoring services strengthen this case.

- Misrepresentation of features: The vendor’s marketing materials promised capabilities the product does not deliver, and refund requests were denied. Email threads comparing promised versus actual functionality support this claim.

- Refund denied in violation of stated policy: The vendor has a published refund or money-back guarantee window but refused to honor it. A screenshot of the policy plus the denial email is typically sufficient evidence.

“Businesses that deliver clear billing transparency and responsive support reduce dispute rates by up to 40%.”

: HubSpot Customer Service Blog

These five scenarios cover the majority of successful SaaS chargebacks. Outside these cases, the vendor’s evidence typically outweighs the cardholder’s claim, and the dispute resolves in the vendor’s favor.

What Are the 5 Limitations of SaaS Chargeback Every Buyer Should Know?

Chargebacks carry real risks for B2B buyers beyond the inconvenience of a 30-to-90-day wait. Vendors retain the right to terminate accounts, flag buyers in fraud databases, and pursue legal action for amounts above card network thresholds. Five limitations define why chargebacks should be a last resort after direct vendor communication has failed.

- Account termination risk: Most SaaS vendors include chargeback-triggered termination clauses in their terms of service. Filing a chargeback against Hunter.io or similar tools typically results in permanent account closure and loss of stored data.

- Time-bound filing window: Chargebacks must be filed within 60 to 120 days of the transaction date, depending on the card network and reason code. Charges outside this window cannot be disputed through the bank regardless of validity.

- No guarantee of success: Vendors with strong documentation, signed terms of service, and usage logs win the majority of disputes. B2B tool vendors routinely track login timestamps, feature usage, and email confirmations as rebuttal evidence.

- Friendly fraud consequences: Filing a chargeback for services actually received, even if disappointing, constitutes friendly fraud. Card issuers track abuse patterns; repeat offenders face credit limit reductions and account restrictions.

- MATCH list exposure: Merchants who lose too many chargebacks report buyers to the Mastercard MATCH (Member Alert to Control High-Risk) list, which can complicate future payment processing for the buyer’s business.

“Reviewing a vendor’s refund policy before subscribing reduces the need for chargebacks by establishing clear expectations upfront.”

: Hunter.io Email Finder review on Growth Hack Suite

These limitations mean chargebacks work best as documented escalation steps, not reflexive responses to billing frustration. Exhausting vendor support and formal refund channels first improves both win rates and buyer standing.

How Has the Concept of SaaS Chargeback Evolved Across the B2B Email Tool Category?

SaaS chargeback disputes in the B2B email tool category have grown more complex as subscription models proliferated. Early SaaS vendors in the 2010s rarely faced chargebacks because enterprise contracts included formal legal dispute clauses. The shift to monthly self-serve subscriptions, starting around 2015, brought a new buyer demographic: SDRs and marketers on company cards who lacked formal procurement processes to challenge billing errors.

By 2020, card networks updated their reason code frameworks to specifically address digital goods and subscription services. Visa’s Reason Code 13.2 and Mastercard’s Reason Code 4853 now explicitly cover “cancelled recurring transactions,” making it easier for buyers to dispute charges after a subscription was supposed to end. Email tool vendors responded by improving cancellation confirmation workflows and adding timestamped audit logs.

The current landscape favors vendors with self-serve cancellation portals, immediate confirmation emails, and published refund windows. Vendors who invested in these systems, including Hunter.io’s subscription management dashboard, see substantially lower chargeback rates than those relying on manual support tickets.

SaaS chargeback evolution reflects a broader market maturation: subscription businesses that treat billing transparency as a product feature, not an afterthought, have structurally lower dispute exposure than those that don’t.

What Are the Real Cost Implications of Implementing SaaS Chargeback at SDR Team Scale?

A single SaaS chargeback costs an SDR team more than the disputed subscription amount. Direct costs include the chargeback fee charged by the payment processor, the administrative time spent gathering evidence, and the cost of replacing the tool if the account is terminated. At scale, teams with three to five email tool subscriptions face compounded risk: disputing one vendor can trigger platform reviews across the entire payment account.

Source: Internal benchmark based on industry-standard SDR hourly rates ($50/hr) and email tool pricing tiers

The math shows that a successful chargeback on a $49 subscription can easily cost $300 to $1,500 in total impact when account replacement and downtime are included. Direct vendor resolution, even when slower, usually delivers better ROI than bank escalation.

What Are the 5 Common Mistakes B2B Teams Make With SaaS Chargeback?

Most failed chargeback attempts in SaaS result from procedural errors made before or during filing, not from weak underlying claims. Five mistakes account for the majority of cases where B2B buyers had legitimate disputes but lost because of how they handled the process.

- Filing before contacting the vendor: Card networks expect buyers to attempt vendor resolution first. Chargebacks filed without prior support contact are consistently weaker, as vendors can show no resolution was requested.

- Missing the filing window: Waiting more than 60 days from the disputed transaction date eliminates most chargeback options. Monthly SaaS billings compound quickly; a six-month-old charge is almost always outside dispute scope.

- Citing the wrong reason code: Selecting “unauthorized transaction” for a subscription the buyer did knowingly sign up for misrepresents the dispute. The correct code is typically “services not as described” or “cancelled recurring billing.”

- Disputing used services: Filing a chargeback for a subscription where the buyer logged in and used the tool constitutes friendly fraud. Usage logs are the vendor’s primary evidence, and they are always available.

- Failing to cancel first: Disputing an active subscription without cancelling it results in continued billing. Vendors win these disputes easily by pointing to the ongoing active account status.

Each mistake is preventable through a simple pre-filing checklist: document the billing error, contact vendor support, request a refund citing the published policy, wait for response, then escalate if refused.

Top 5 Tools Compared by SaaS Chargeback Policy: Hunter, Apollo, Snov, ZeroBounce, NeverBounce

Email tool vendors vary significantly in their refund and dispute policies, which directly affects how often chargebacks become necessary. Tools with published money-back windows, self-serve cancellation, and responsive billing support see fewer bank disputes. The comparison below covers the five tools most commonly used by SDR teams and email marketers, ranked by their overall chargeback-friendliness.

Source: Vendor terms of service pages and support documentation reviewed May 2026. Policies subject to change.

Hunter.io and Snov.io offer the clearest refund pathways, making chargebacks a genuine last resort rather than a frequent necessity. Tools with vague or credit-only policies create conditions where chargebacks become the only viable cash recovery option.

How Do SDRs, Email Marketers, and Founders Each Apply SaaS Chargeback Differently?

The decision to file a SaaS chargeback looks different depending on who is managing the subscription and what their relationship with the tool is. Three personas dominate SaaS chargeback scenarios in the B2B email tool category, and each faces a distinct risk-benefit calculation when a billing dispute arises.

SDRs on company cards file chargebacks most frequently because they often subscribe to tools independently, without formal procurement review. SDRs using tools like Hunter.io for a single outreach campaign may cancel after one month and then receive unexpected renewal charges. For SDRs, chargebacks are often the fastest path to recovery, but account termination means losing the verified email database and campaign history they built during the subscription.

Email marketers typically have longer vendor relationships and more complex integrations. An email marketer who has connected Hunter.io to their CRM and built prospect lists faces a much higher switching cost from chargeback-triggered termination. Marketers are more likely to escalate through formal refund requests and only consider chargebacks for clear billing errors like duplicate charges.

Founders and solopreneurs use chargebacks selectively for high-value disputes, typically on annual plan renewals above $200. Founders are most sensitive to the MATCH list risk and account termination consequences, since their personal and business cards are often linked. A founder disputing a Hunter.io annual renewal will typically exhaust every vendor channel before filing with the bank.

Persona context determines the right escalation threshold. The common denominator across all three is: document everything, contact vendor support first, and treat the chargeback as a last resort rather than a first response.

How Do You Apply SaaS Chargeback in 5 Steps with Hunter.io (Free Workflow)?

When Hunter.io or any SaaS vendor bills in error and refuses to resolve the issue through direct support, a structured five-step chargeback workflow maximizes the chance of a favorable bank ruling while minimizing account termination exposure. This workflow applies to all credit card networks and all SaaS subscription types.

- Step 1, document the billing error: Screenshot the charge on your bank statement, the vendor invoice, and any cancellation confirmations or plan change records. Timestamped evidence is the foundation of every successful dispute.

- Step 2, contact Hunter.io support via the billing channel: Email billing@hunter.io or open a support ticket through the Hunter dashboard. Reference the specific charge date, amount, and the reason the charge is disputed. Keep all correspondence.

- Step 3, request a formal refund citing the published policy: Hunter.io’s refund policy allows pro-rated refunds within 30 days. Cite the policy URL in your message and request written confirmation of the refund timeline.

- Step 4, wait the stated response window before escalating: Give Hunter.io 5 to 7 business days to respond. If the refund is denied or no response is received, send a final written escalation citing the policy breach.

- Step 5, file the chargeback with evidence packet: Contact your card issuer and cite Reason Code 13.2 (cancelled recurring) or 13.3 (services not as described). Submit the billing documentation, vendor correspondence, and refund denial as your evidence packet.

Need a billing resolution? Start with Hunter.io’s free plan first.

Try Hunter.io FreeFree plan includes 25 searches/month. No credit card required.

This five-step workflow works because card networks evaluate whether buyers attempted good-faith resolution before escalating. A documented vendor refusal is far stronger evidence than a unilateral bank dispute with no prior vendor contact.

What Are the Best Practices for Implementing SaaS Chargeback in Your B2B Stack?

Systematic chargeback prevention starts before a billing dispute occurs. B2B teams that build simple subscription management habits eliminate the conditions where chargebacks become necessary. Five best practices cover the full lifecycle from subscription to cancellation to dispute escalation.

- Read the refund policy before subscribing: Vendors with published 30-day refund windows, like Hunter.io, offer meaningful protection. Vendors with credit-only policies or no stated window require more caution before committing to annual plans.

- Use a dedicated company card for SaaS: Isolating SaaS subscriptions to one card simplifies dispute management and protects personal credit from chargeback exposure. Virtual cards with per-merchant spending limits add another layer of control.

- Maintain a subscription register: A simple spreadsheet tracking vendor, billing date, renewal amount, and cancellation deadline prevents accidental renewals. Review the register monthly before renewal dates hit.

- Cancel in writing before the renewal date: Cancellation confirmation emails are the most powerful evidence against unauthorized renewal charges. Cancel at least 48 hours before the renewal date and save the confirmation email with timestamp.

- Escalate in sequence, not simultaneously: Contact vendor support, then request a formal refund, then escalate to the bank. Filing a chargeback while vendor resolution is still pending weakens the case and increases the chance of a lost dispute.

Teams that follow these practices rarely need to file chargebacks because they either prevent billing errors or resolve them through vendor channels before the bank dispute window becomes necessary.

What Industry Trends Are Reshaping SaaS Chargeback Going Into Late 2026?

Three converging trends are changing how SaaS chargebacks are filed, adjudicated, and prevented across the B2B email tool market. Understanding these shifts helps SDR teams and marketers anticipate where their billing rights are expanding and where vendor defenses are becoming more sophisticated.

AI-powered chargeback detection by vendors. Email tool vendors are deploying machine learning models that flag high-risk cancellation patterns and proactively reach out to customers before they file disputes. Hunter.io and similar tools with usage analytics can identify accounts that have stopped using the product mid-cycle and offer proactive downgrades or refunds before the customer contacts their bank.

Card network rule tightening on digital goods. Visa and Mastercard updated their chargeback rules for digital goods and SaaS subscriptions in 2024 and again in 2025. The updates reduced the dispute window for some subscription categories to 60 days and added requirements for vendors to show evidence of account access logs, not just payment confirmation.

Subscription management tools as chargeback prevention. Platforms like Paddle, Stripe Billing, and Chargebee now include built-in dispute prevention features: smart dunning, self-serve cancellation portals, and automatic chargeback evidence collection. Vendors using these platforms can respond to disputes in hours rather than days, significantly improving their win rates.

The net effect of these trends is a more structured dispute environment where documentation quality and response speed determine outcomes more than the underlying claim merit. B2B buyers and vendors alike benefit from clearer processes and faster resolutions.

Avoid billing disputes with a tool that publishes its refund policy.

Hunter.io offers a 30-day pro-rated refund and self-serve cancellation. Start free, upgrade only when you need more searches.

Get Started with Hunter.io FreeFree plan: 25 searches/month. Paid from $49/month. Cancel anytime.

SaaS Chargeback: Frequently Asked Questions

What is a SaaS chargeback?

A SaaS chargeback is a bank-enforced payment reversal where a cardholder disputes a charge from a software vendor through their credit card issuer. The bank investigates, temporarily credits the cardholder, and gives the vendor time to respond with evidence. If the vendor cannot prove the charge was valid, the reversal becomes permanent and the vendor also pays a chargeback fee.

How is a chargeback different from a refund?

A refund is voluntary: the vendor decides to return funds. A chargeback is involuntary: the bank takes funds from the vendor without their consent. Refunds preserve the vendor relationship; chargebacks typically trigger account termination. Refunds process in 3 to 10 business days; chargebacks take 30 to 90 days. Always request a refund first and use chargebacks only when the vendor refuses.

When is it justified to file a SaaS chargeback?

Five scenarios justify a SaaS chargeback: billing after cancellation, duplicate charges, service not delivered, misrepresentation of features, and refund denied despite a published policy. Filing for any other reason, including dissatisfaction with a tool you used, constitutes friendly fraud. Always document vendor refusal before contacting the bank.

How long do you have to file a SaaS chargeback?

The standard chargeback window is 60 to 120 days from the transaction date, depending on the card network and dispute reason code. Visa generally allows 120 days for most dispute types. Mastercard uses 120 days for most categories but 60 days for certain digital goods. Charges outside this window cannot be disputed through the bank regardless of how valid the claim is.

Can filing a chargeback get your SaaS account terminated?

Yes. Most SaaS vendors, including email tools like Hunter.io, include chargeback-triggered termination clauses in their terms of service. Once a chargeback is filed, vendors typically close the account immediately, regardless of the dispute outcome. Account termination means losing stored data, email lists, campaign history, and API integrations. This is the primary reason chargebacks should be a genuine last resort.

What evidence do you need to win a SaaS chargeback?

Strong chargeback evidence includes: the original billing statement showing the disputed charge, cancellation confirmation with timestamp, vendor correspondence showing refund was refused, a screenshot of the published refund policy, and any service downtime records if disputing non-delivery. The more specific the documentation, the lower the vendor’s ability to rebut. Vague complaints without paper trails lose consistently.

Will a SaaS chargeback affect your credit score?

A single legitimate chargeback does not affect your personal credit score. Card issuers do not report chargeback disputes to credit bureaus. However, repeat chargebacks, particularly ones the cardholder loses, can lead the card issuer to flag the account, reduce credit limits, or close the card. Abuse of the chargeback process is tracked internally by issuers even when it doesn’t appear on a credit report.

How long does a SaaS chargeback dispute take to resolve?

Most SaaS chargeback disputes resolve in 30 to 90 days. The bank provides a provisional credit within 1 to 5 business days of the dispute being filed. The vendor then has 20 to 45 days to respond with evidence. After both sides submit documentation, the card network issues a final ruling. Complex disputes can extend to 120 days if either party files an arbitration request.

What happens to the SaaS vendor when a chargeback is filed?

The vendor’s payment processor deducts the disputed amount plus a chargeback fee of $25 to $100 per dispute. The vendor has 20 to 45 days to submit a rebuttal with evidence. If the vendor’s chargeback rate exceeds 1% of monthly transactions, Visa or Mastercard enrolls them in a monitoring program with additional fees. Exceeding 2% can result in payment processing account termination for the vendor.

Does Hunter.io have a chargeback-friendly refund process?

Hunter.io offers a 30-day pro-rated refund policy, meaning subscribers can request a refund within 30 days of any billing cycle and receive credit for unused time. Cancellation is self-serve through the account dashboard. This policy reduces the need for chargebacks to genuine billing errors. Contacting Hunter’s billing support at billing@hunter.io and citing the published policy typically resolves disputes without bank escalation.

Can you file a chargeback if you forgot to cancel a SaaS subscription?

Forgetting to cancel does not justify a chargeback unless the vendor failed to send renewal reminders as required by their stated policy or applicable consumer protection laws. Most SaaS subscriptions send renewal notifications 7 to 30 days in advance, and card networks expect buyers to manage their own subscriptions. Filing a chargeback for a valid renewal you simply forgot about is likely to be denied.

What is friendly fraud in SaaS chargebacks?

Friendly fraud occurs when a cardholder disputes a legitimate charge, either claiming non-delivery for a service they used or denying authorization for a subscription they knowingly purchased. In SaaS, friendly fraud typically involves disputing a monthly tool charge after using it all month. Card issuers track this behavior, and repeat friendly fraud can result in account closures and restrictions on the buyer’s credit card.